Retail banking software development is the process of designing and building the digital systems that power consumer banking: core banking engines, mobile and web banking apps, KYC/AML compliance modules, payment processing, and open banking APIs. The global AI in banking market was valued at $34.58 billion in 2025 and is projected to reach $379.41 billion by 2034 at a 38.28% CAGR. Development costs range from $50,000 for a basic mobile banking app to $2 million or more for a full core banking platform. Decipher Zone has delivered retail and fintech banking platforms for clients in Africa, the US, and the Gulf region.

Banking is the most regulated, most security-critical sector in software development. A bug in an ecommerce checkout is an inconvenience. A bug in a core banking transaction ledger is a financial crisis.

The number of digital banking users is projected to reach 3.6 billion globally, and by 2026 an estimated 90% of all banking interactions will occur through digital channels. The third-party banking software market was valued at $31.08 billion in 2024 and is expected to reach $57.96 billion by 2032.

This guide covers what retail banking software is, why banks and fintech startups invest in it, the core features and technology stack, compliance requirements, development costs, 2026 trends, and how Decipher Zone approaches these projects based on real client work.

Read: Fintech Software Development | Future of Fintech | Mobile App Development

What Is Retail Banking Software?

Retail banking software is the enterprise software suite that banks use to manage consumer-facing financial products and day-to-day transactions. It is the digital backbone enabling retail banks to offer savings and checking accounts, loans, credit cards, and payment processing to the public.

This software encompasses everything from back-end systems that handle account management and transaction ledgers to front-end applications that customers use for online and mobile banking.

At its core, retail banking software must reliably record every customer transaction in real time and in compliance with strict regulations. It provides the infrastructure to create, deploy, and manage financial products while storing sensitive customer data securely in line with local banking laws.

Modern retail banking platforms also power the user interfaces for ATMs, branch tellers, internet banking portals, and mobile apps, effectively the face and feel of a bank's services in the digital realm.

Neobank vs Traditional Bank Software: Key Differences

Understanding the architectural difference between neobank and traditional bank software helps developers and executives make better build decisions in 2026.

| Aspect | Traditional Bank Software | Neobank Software |

|---|---|---|

| Core architecture | Monolithic or legacy mainframe | Cloud-native microservices |

| Deployment speed | 18 to 24 months for new features | 3 to 6 months MVP to launch |

| Scalability | Manual capacity planning required | Auto-scaling on cloud infrastructure |

| API openness | Limited, often proprietary | API-first, open banking ready |

| Compliance tooling | Manual reporting, separate systems | Automated, embedded in workflows |

| User experience | Branch-first, digital as supplement | Mobile-first, branch-free design |

| Cost structure | High infrastructure, low variable | Low fixed, pay-as-you-grow |

| Integration model | Tight coupling with third parties | Loosely coupled via REST and webhooks |

5 Reasons to Invest in Retail Banking Software Development

1. Digital-First Customer Behavior

Consumers increasingly prefer digital channels for every banking interaction. Globally, the number of digital banking users is projected to reach 3.6 billion, and by 2026 an estimated 90% of all banking interactions will occur through digital channels. From mobile check deposits to online loan applications, customers expect on-demand 24/7 access. Retail banking software is the engine that provides this always-on convenience.

2. Competitive Pressure from Fintechs and Neobanks

Agile fintech companies and digital-only neobanks are quick to deploy innovative financial products and personalized user experiences. 82% of traditional banks plan to increase partnerships with fintech companies in the next three to five years. A flexible software architecture with open APIs and modular services is essential to enable such collaborations and embedded finance models.

3. Post-Pandemic Digital Transformation

The COVID-19 pandemic accelerated digital adoption in banking permanently. Over 1,600 US bank branches close per year on average as digital alternatives grow. Cloud-based core systems, contactless payments, and remote customer onboarding have moved from "nice to have" to "must have" in 2026. Retail banking software is the cornerstone of this transformation.

4. Regulatory Compliance and Security

As banking goes digital, regulators worldwide enforce strict standards for data security, privacy, and financial integrity. Global penalties for AML and KYC compliance failures surged 57% in 2023, reaching into the billions. Modern built-in compliance management automates checks, flags suspicious activities, and generates audit trails.

5. Personalization and AI-Driven Customer Experience

Banks are realizing that technology is key to delivering personalized service at scale. 79% of banks agree that customers want human-like AI interactions in digital banking. 40% of users are willing to pay for personalized digital banking services. Features like intelligent chatbots, virtual financial advisors, and predictive financial insights are becoming standard in every retail banking platform.

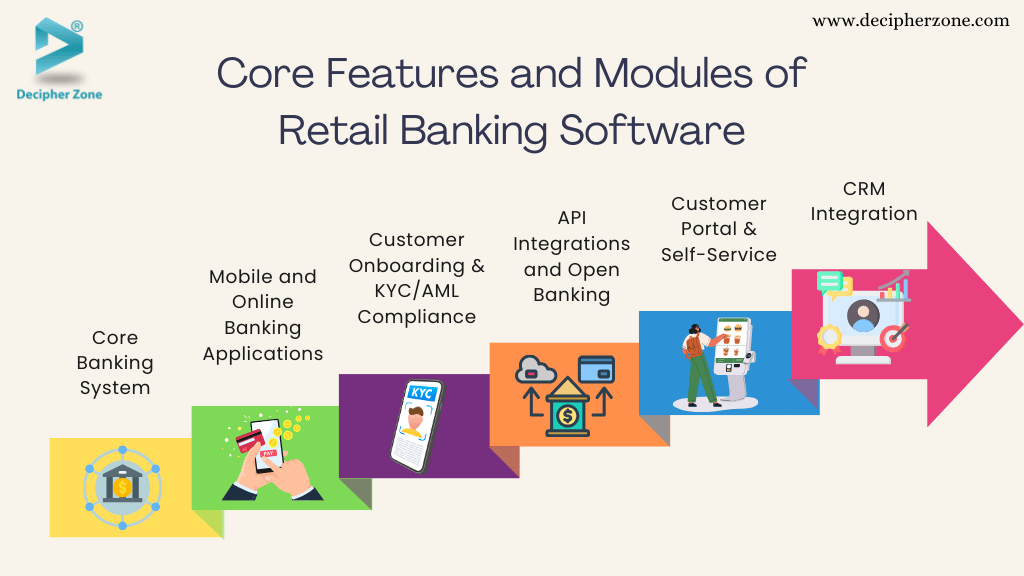

Core Features and Modules of Retail Banking Software

1. Core Banking System

What It Does

The core banking system ensures that when a customer makes a transaction (a fund transfer, loan payment, or deposit), it is recorded in real time, updating all relevant balances across the bank instantly. It is the single source of truth for all customer financial data.

Key Capabilities

- Multi-currency transactions and real-time gross settlement

- End-of-day batch processing for reconciliation

- High availability architecture with no single point of failure

- Account lifecycle management from opening to closure

- Interest calculation engines for savings, loans, and deposits

- General ledger integration for financial reporting

2. Mobile and Online Banking Applications

What It Does

These are the customer-facing portals (mobile apps and web banking sites) that allow users to interact with the bank digitally. Through these apps, customers check balances, transfer money, pay bills, deposit checks via photo, apply for accounts or loans, and chat with support.

Key Capabilities

- Consistent intuitive UI/UX across mobile and web channels

- Push notifications for real-time transaction alerts

- Biometric login via fingerprint and face recognition

- Personalized dashboards with spending analytics

- In-app customer support with chatbot and live agent handoff

- Peer-to-peer payment flows with contact integration

3. Customer Onboarding and KYC/AML Compliance

What It Does

A crucial module that manages enrolling new customers and verifying their identity. KYC (Know Your Customer) and AML (Anti-Money Laundering) features collect customer information, verify IDs via document upload or biometric checks, and screen for fraud or sanctions lists automatically.

Key Capabilities

- Document scanning with AI-powered OCR and liveness detection

- Real-time sanctions screening against OFAC, EU, and UN watchlists

- Ongoing transaction monitoring with risk-based rule engines

- Suspicious activity report (SAR) generation for regulators

- Customer risk scoring updated on each new transaction event

- Video KYC for fully remote account opening workflows

4. API Integrations and Open Banking

What It Does

Modern banking software exposes APIs that allow secure integration with external services and fintech apps. This module manages API gateways, authentication, and data exchange protocols. It connects the bank to payment networks (Visa, Mastercard), fintech products, credit bureaus, and the FedNow instant payment rail launched in 2023.

Key Capabilities

- RESTful and GraphQL API endpoints with OAuth 2.0 and OpenID Connect

- PSD2-compliant open banking data sharing for EU markets

- ISO 20022 message format support for cross-border payment compliance

- Webhook delivery for real-time event notifications to third parties

- API rate limiting, versioning, and developer portal with documentation

- Banking-as-a-Service (BaaS) module for embedded finance products

5. Customer Portal and Self-Service

What It Does

Beyond transactional banking, retail banking software includes a full customer portal where users manage their entire relationship with the bank. This is the one-stop hub for updating profiles, requesting services, tracking application status, and downloading statements.

Key Capabilities

- Support ticketing with SLA tracking and escalation routing

- Product dashboards for loans, investments, and credit cards

- Document upload and download for statements and agreements

- Loan application tracking with real-time status updates

- Communication preferences and notification management

6. CRM Integration

What It Does

CRM integration tracks customer interactions across all channels, stores profiles and preferences, and helps banks analyze customer behavior. Bank staff use CRM data to see a customer's entire history at a glance, enabling proactive service and cross-sell opportunities.

Key Capabilities

- 360-degree customer view combining transactional and behavioral data

- Automated product recommendations based on customer lifecycle stage

- Relationship manager dashboards for high-value customer segments

- Campaign management for targeted financial product offers

7. Compliance and Risk Management

What It Does

In addition to KYC/AML, broader compliance management features cover regulatory reporting, internal audit trails, risk scoring, and policy enforcement. The software generates reports required by regulators at the push of a button and enforces credit risk limits automatically.

Key Capabilities

- BASEL III capital adequacy calculation and reporting

- IFRS 9 expected credit loss modeling for loan portfolios

- Real-time liquidity risk monitoring with threshold alerts

- Automated regulatory filing for central bank submissions

- Immutable audit trails with timestamp-stamped access logs

Compliance Framework Requirements for Retail Banking Software

Every retail banking software project must address multiple overlapping regulatory frameworks simultaneously. The compliance table below covers the frameworks your development team must build for, depending on your geographic markets and product types.

| Framework | Scope | Key Technical Requirements | Penalty for Failure |

|---|---|---|---|

| PCI DSS | Card payment data handling | Encryption, tokenization, network segmentation, annual penetration tests | $5,000 to $100,000 per month plus card network fines |

| GDPR | EU personal data | Consent management, data minimization, right to erasure, 72-hour breach notification | Up to 4% of global annual turnover |

| SOC 2 | US service providers | Security, availability, processing integrity, confidentiality, privacy controls | Loss of enterprise contracts, reputational damage |

| PSD2 | EU payment services | Strong customer authentication (SCA), open banking APIs, third-party access | Regulatory sanctions and market exclusion |

| BSA/AML | US financial institutions | Customer identification, SAR filing, transaction monitoring, sanctions screening | $1M+ per day for willful violations |

| FFIEC | US bank IT governance | OAuth 2.0, OpenID Connect, step-up authentication, audit logging | Formal enforcement actions, consent orders |

| ISO 20022 | Cross-border payments | Structured message formats, rich remittance data, phased migration by 2026 | Inability to process international payments |

Read: Cybersecurity Trends 2026 | Cybersecurity Best Practices | Enterprise Risk Management Software

Technology Stack for Retail Banking Software Development

Developing a robust retail banking platform requires choosing the right technologies and architectural approaches. The table below compares the primary backend languages used in banking software, a comparison that no other guide in the top search results currently provides.

| Technology | Best For | Banking Strengths | Considerations |

|---|---|---|---|

| Java + Spring Boot | Core banking, transaction engines | Strong type safety, mature ecosystem, excellent backward compatibility, HIPAA/PCI tooling | Higher initial development cost, verbose code |

| Python | AI/ML models, fraud detection, analytics | Fastest ML library ecosystem, rapid prototyping, excellent data pipeline tooling | Not ideal for high-concurrency transaction processing |

| Node.js | API gateways, real-time notifications | High throughput for I/O-bound operations, fast development, great for BaaS APIs | Less mature for complex financial calculations |

| .NET (C#) | Enterprise banking platforms | Strong Microsoft Azure integration, enterprise support, Windows-compatible legacy systems | Higher licensing cost in some configurations |

| React / React Native | Mobile and web banking apps | Cross-platform code reuse, large talent pool, excellent component ecosystems | Requires separate native modules for biometrics |

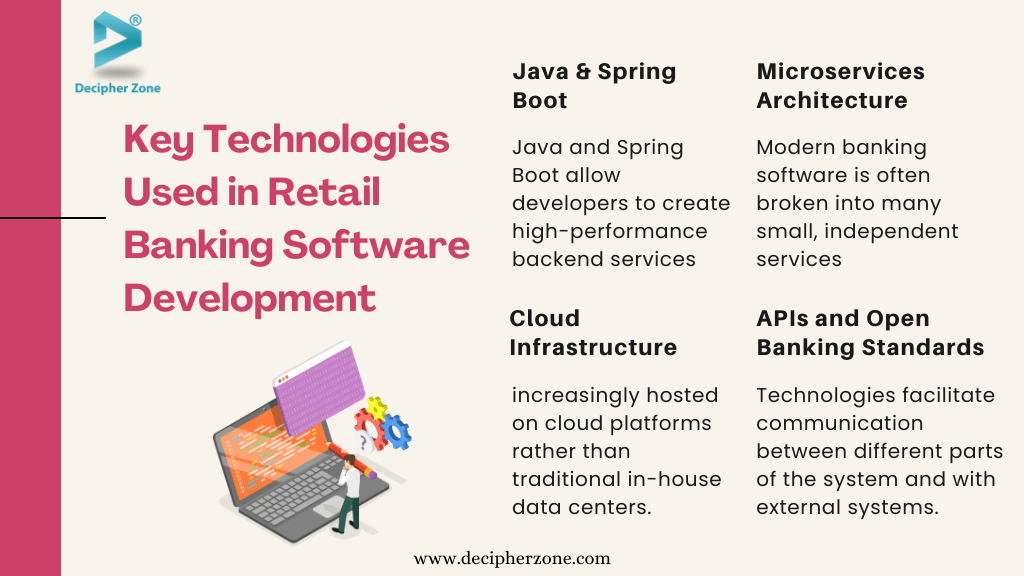

1. Java and Spring Boot

Java remains a cornerstone of banking software development due to its reliability, performance, and strong security features. Many core banking systems are built in Java, leveraging its vast ecosystem of libraries and enterprise tools.

Spring Boot accelerates development by providing ready-made configurations for microservices, web services, and database access. These technologies are also known for excellent backward compatibility, which is crucial for banking systems that need to run for years and integrate with older infrastructure.

2. Microservices Architecture

Instead of one giant application, modern banking software is broken into many small independent services. Each microservice handles a specific function: a service for managing customer profiles, another for payments, another for loans.

This architecture allows scaling parts of the system independently and enables parallel development by different teams. Technologies like Docker and Kubernetes are used to deploy and manage microservices in production.

3. Cloud Infrastructure

Retail banking software is increasingly hosted on cloud platforms rather than traditional in-house data centers. Cloud providers like AWS and Microsoft Azure offer robust infrastructure with global data centers, high availability, and compliance certifications.

Many modern banking solutions use a hybrid cloud approach: critical data resides on a private cloud or secure on-premise server, while front-end services run on public cloud to balance security and cost.

4. APIs and Open Banking Standards

Technologies like RESTful web services, GraphQL, and Apache Kafka for real-time data streaming are fundamental to modern banking software. By adhering to standardized APIs including ISO 20022 for payment messaging and PSD2 open banking standards, banking software can more easily plug into payment networks and third-party services without custom integration work for each connection.

.avif)

5. Blockchain for Banking

Blockchain is used selectively in banking for its strengths in security and transparency. Private permissioned blockchains using frameworks like Hyperledger Fabric or Corda improve processes like cross-border payments and trade finance.

Blockchain-based digital identity creates immutable audit trails that are attractive for fraud detection and regulatory compliance. As central bank digital currencies (CBDCs) and tokenized assets become mainstream, blockchain components will play a larger role in next-generation retail banking systems.

6. DevOps and CI/CD

Technologies under the DevOps umbrella (Jenkins, GitLab CI, Azure DevOps) automate testing and deployment of banking applications. Given the need for zero downtime updates and rigorous testing, where any bug can have direct financial implications, DevOps is not optional in banking. Automated pipelines run unit tests, integration tests, and security scans every time new code is pushed, ensuring only high-quality code reaches production.

7. Security Technologies

Every layer of the banking tech stack is configured with security as a primary constraint, not an afterthought:

- AES-256 encryption for data at rest and TLS 1.2+ for data in transit

- Hardware security modules (HSMs) for encryption key management

- Field-level encryption so database administrators cannot read payment details in plain text

- Tokenization replacing card numbers (PANs) with non-sensitive tokens throughout systems

- Keycloak or similar IAM tools for secure coding and role-based access control

- OWASP top 10 vulnerability scanning embedded in CI/CD pipelines

Retail Banking Software Development Costs in 2026

Development cost is one of the most searched topics in this space and the dimension that no comprehensive guide currently provides in full detail. The table below breaks down realistic cost ranges by project type, based on Decipher Zone's delivery experience across banking and fintech projects.

| Project Type | Scope | Timeline | Estimated Cost |

|---|---|---|---|

| Basic mobile banking app | Account view, transfers, bill pay, push notifications, biometric login | 4 to 6 months | $50,000 to $150,000 |

| Full digital banking platform | Mobile app + web portal + KYC/AML + card management + customer support | 8 to 14 months | $200,000 to $600,000 |

| BaaS / fintech API platform | API gateway, open banking integrations, developer portal, compliance module | 10 to 16 months | $300,000 to $800,000 |

| Core banking system | Transaction ledger, account management, product engine, reporting, risk module | 12 to 24 months | $800,000 to $2,000,000+ |

| Neobank MVP | Cloud-native core, mobile app, KYC, basic payments, operations dashboard | 6 to 10 months | $150,000 to $400,000 |

| Compliance module only | KYC automation, AML monitoring, regulatory reporting, audit trails | 3 to 6 months | $80,000 to $250,000 |

At Decipher Zone, senior engineers work at $25 to $49 per hour. Every banking project begins with a discovery phase to scope architecture and compliance requirements before production development starts, which prevents the budget overruns that occur when compliance gaps are discovered mid-build.

Read: Financial Software Development Cost Guide | Fintech App Development | How to Develop Software from Scratch

Benefits for Banks

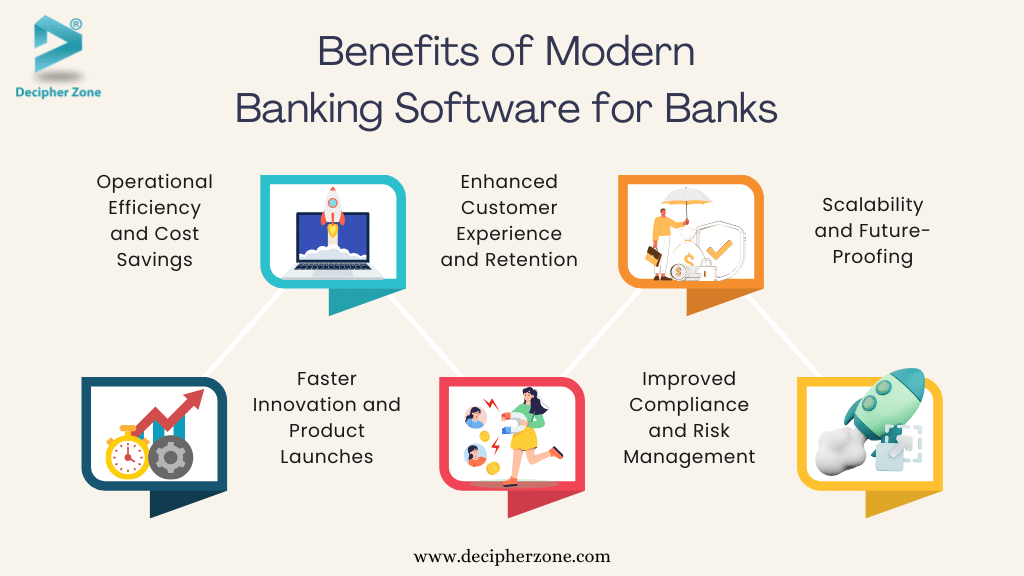

1. Operational Efficiency and Cost Savings

Automating banking processes through modern software reduces manual work, errors, and processing time. Routine transactions that once required paperwork and branch visits are now handled instantly online. Modern core systems deliver lower operating costs, faster service delivery, and the ability to reallocate staff from transaction processing to relationship management and advisory services.

2. Faster Innovation and Product Launches

A flexible microservices architecture with open APIs lets banks develop and deploy new products rapidly. Instead of months of coding on a monolithic legacy system, banks can use modular services to roll out a new mobile payment feature or a fintech partner integration in weeks. Modern retail banking software removes the roadblocks that historically made even simple feature additions a six-month project.

3. Enhanced Customer Experience and Retention

With a 360-degree digital platform, banks provide a smooth and personalized customer journey. A customer could start a loan application online and finish it in a branch without restarting the process. 76% of online banking users are satisfied with their digital experience, and satisfaction leads directly to loyalty and reduced churn.

4. Improved Compliance and Risk Management

Advanced banking software automates compliance tasks and provides better oversight across all operations. Risk management tools monitor credit risk in real time, alerting management to portfolio issues before they become crises. With compliance built into daily workflows rather than bolted on at reporting time, banks maintain stability and can reassure regulators with audit-ready documentation on demand.

5. Scalability and Future-Proofing

Cloud-native core banking systems handle growth effortlessly. If a bank's user base doubles, auto-scaling resources accommodate the surge without the manual capacity planning that older systems require. By using updatable software components, banks can adopt future technologies including CBDCs, new payment rails, and blockchain for settlement without rebuilding the platform from scratch.

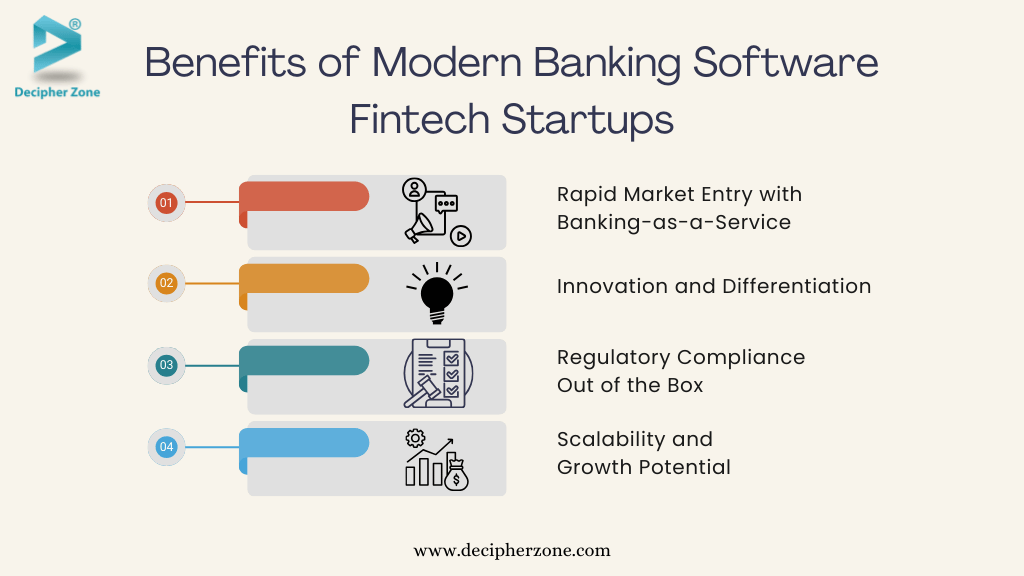

Benefits for Fintech Startups

1. Rapid Market Entry with Banking-as-a-Service

Fintech startups can integrate with a BaaS platform that provides core banking functions (account ledger, compliance checks, card issuance) via APIs, allowing the fintech to offer customers bank-like services under its own brand without building everything from scratch. The startup focuses on its unique user experience while the proven banking software handles regulatory compliance, transaction processing, and security.

2. Innovation and Differentiation Through Modular Architecture

By leveraging modern banking software components, fintechs can combine services to create innovative offerings. APIs and modular banking services make it possible to bundle a budgeting app with a debit card and a crypto wallet on a single platform. Fintechs benefit from microservices architectures that let them use only the features they need and customize the rest, enabling differentiation with niche features like an AI-powered financial coach or a unique rewards system.

3. Compliance Ready from Day One

Using an established retail banking software with pre-packaged KYC workflows, fraud detection algorithms, and reporting functions gives fintech startups a compliance-ready framework without building it independently. For a startup, this is invaluable: it ensures they do not inadvertently run afoul of laws and it builds trust with users who would otherwise worry about the safety of their money with a new player.

4. Scalability from 5,000 to 5 Million Users

A well-architected banking backend accommodates growth from beta to mainstream without performance degradation. Many banking platforms include multi-currency and multi-country support, so a fintech can expand services internationally by toggling on new modules (subject to partnerships and licenses) rather than rebuilding for each new market.

Retail Banking Software Development Trends in 2026

1. Agentic AI and Hyperautomation

The global AI in banking market is projected to grow from $34.58 billion in 2025 to $379.41 billion by 2034 at a 38.28% CAGR. In 2026, AI is deeply integrated into fraud detection, credit scoring, personalized financial planning, and customer onboarding.

Hyperautomation, which combines AI, RPA (robotic process automation), and data analytics, is being used to automate everything from compliance checks to loan processing workflows without human intervention at each step.

2. Central Bank Digital Currencies (CBDCs)

Over 130 countries are now exploring or piloting CBDCs. Retail banks and fintech platforms must prepare their software architectures to support CBDC wallets, settlement rails, and programmable money use cases. This requires API-first core banking systems and blockchain-capable infrastructure that can integrate with central bank systems as these digital currencies move from pilot to mainstream.

3. Embedded Finance

Embedded finance allows non-banking brands (retailers, logistics companies, healthcare platforms) to offer financial services directly within their own products. The underlying technology is BaaS APIs from banking software platforms. In 2026, banks that expose well-designed APIs to third parties generate significant non-interest revenue from usage fees while expanding their effective customer base without the cost of direct customer acquisition.

4. Low-Code and No-Code Banking Platforms

Low-code platforms allow banks to build applications using visual interfaces and pre-built templates, drastically reducing development time for non-core banking features. In 2026, banks use low-code tools to rapidly deploy regional compliance modules, internal workflow tools, and customer portals while reserving custom development for the transaction-critical core systems where performance and security requirements exceed what low-code platforms can guarantee.

5. Real-Time Payments and ISO 20022 Migration

The US Federal Reserve launched FedNow in 2023, enabling instant payments 24 hours a day, 7 days a week. The ongoing global migration to ISO 20022 payment messaging standards is pushing banks worldwide to update their payment processing infrastructure.

Retail banking software built in 2026 must support multiple payment rails simultaneously: ACH, FedNow, SWIFT, SEPA, and local payment schemes, with ISO 20022 structured message formats for all cross-border transactions.

6. Biometric Authentication and Passwordless Banking

Biometric authentication has become the customer expectation, not a premium feature. Face recognition, fingerprint scanning, and behavioral biometrics (typing patterns, device handling) are now baseline security requirements for mobile banking apps.

Combined with FIDO2 passkey standards, passwordless banking eliminates the largest single attack vector in digital banking, credential theft, while improving user experience.

Read: Technologies Shaping the Future of Fintech | Cloud Computing Trends | AI Enabled Software Development

Decipher Zone's Approach to Retail Banking Software Development

1. Deep Domain Expertise and Consultation

We begin by truly understanding the client's needs, whether it is a traditional bank modernizing its core system or a fintech startup building a new platform. Our team includes experts with experience in banking operations, compliance, and fintech innovation.

We speak the language of banking, from regulatory acronyms to industry best practices, so our development plans are rooted in real-world knowledge that reduces compliance surprises mid-project.

2. Customer-Centric and People-First Design

Our approach emphasizes intuitive UI/UX design and smooth customer journeys. In one project we integrated an AI-driven chatbot to guide users through onboarding, reducing drop-offs.

In another, we implemented real-time notifications and personal finance dashboards based on user feedback. By keeping end-users at the center, Decipher Zone builds banking applications that drive higher adoption and satisfaction.

3. Agile Development with Rigorous Quality Assurance

Banking requirements can evolve with market changes or feedback, so our development process is agile and iterative. We break projects into sprints, delivering incremental features for review.

Throughout development, every build goes through extensive testing: functional tests, integration tests, performance benchmarking, security audits, and User Acceptance Testing (UAT) with client stakeholders.

4. Security-First Engineering

Trust is the currency of banking, and we embed security at every layer. Decipher Zone follows secure coding standards and leverages robust security frameworks. For Tag Biometrics, we implemented unique encryption tokens for each card and integrated Keycloak for authentication.

Our approach includes regular code reviews focused on security, penetration testing, OWASP compliance checks, and data architecture that supports GDPR and PCI-DSS requirements from day one.

5. Scalable and Future-Ready Architecture

We architect solutions with a long-term perspective using microservices and cloud deployment. When we built the APIs and microservices for a client with extensibility in mind, adding a digital wallet feature a year after initial launch was seamless because the architecture had already anticipated it.

We provide training and documentation as part of every project handoff, empowering clients to manage and extend the product after delivery.

6. Measurable Results and Continuous Improvement

We define KPIs for success at the project start (system uptime, transaction processing speed, user growth, customer satisfaction) and architect to meet those metrics. After deployment, we monitor performance and implement improvements based on real usage data.

In one case, gathering user feedback post-launch led us to implement a one-click payment rescheduling feature that measurably improved convenience scores in the client's satisfaction surveys.

Case Studies: Real Banking Projects from Decipher Zone

Letshego: Microfinance and Digital Banking in Africa

The Challenge

Letshego is a prominent microfinance and banking institution operating across multiple African countries, focused on delivering inclusive finance (small loans, savings, and payments) to underserved communities. They needed a digital banking platform that could work in low-bandwidth rural environments while scaling to national usage volumes.

What We Built

- Mobile wallet app with offline transaction queuing for low-connectivity regions

- Agent banking portal for community-level banking representatives

- Core service integrations for loan processing and bill payments

- AWS and Azure cloud hosting with Kubernetes containerization for peak-load scaling

.avif)

The Outcome

People in remote areas can now open accounts and perform transactions via their phones without needing a physical bank branch. The platform scales smoothly during monthly loan disbursement cycles, and Kubernetes containerization handles peak usage without manual intervention. Thousands of individuals and small businesses now access reliable banking services aligned with Letshego's financial inclusion mission.

BLAZE: ERP and Point-of-Sale for Cannabis Financial Services

The Challenge

The Challenge

BLAZE is a specialized financial software suite for the cannabis dispensary industry, offering point-of-sale, inventory management, and compliance tracking. Cannabis retailers face unique financial and regulatory challenges, including state-level compliance reporting requirements and the need to eliminate cash-only operations.

What We Built

- React.js mobile POS application for dispensary staff (tablet-optimized)

- Java 8 and Dropwizard backend with MongoDB for flexible data storage

- Stripe integration for digital payments and Twilio for SMS notifications

- Digital signature capture eliminating paper forms

- AES-256 encryption for all data at rest

- Metrc compliance integration for mandatory state reporting

The Outcome

Dispensary staff now sign up members, verify age and identity, and complete sales on an intuitive tablet app with customer wait times reduced. New customers complete all required agreements digitally on iPad with secure storage compliant with state laws. The system automatically logs each sale with required compliance data, keeping the business in good standing with regulators while eliminating manual paperwork entirely.

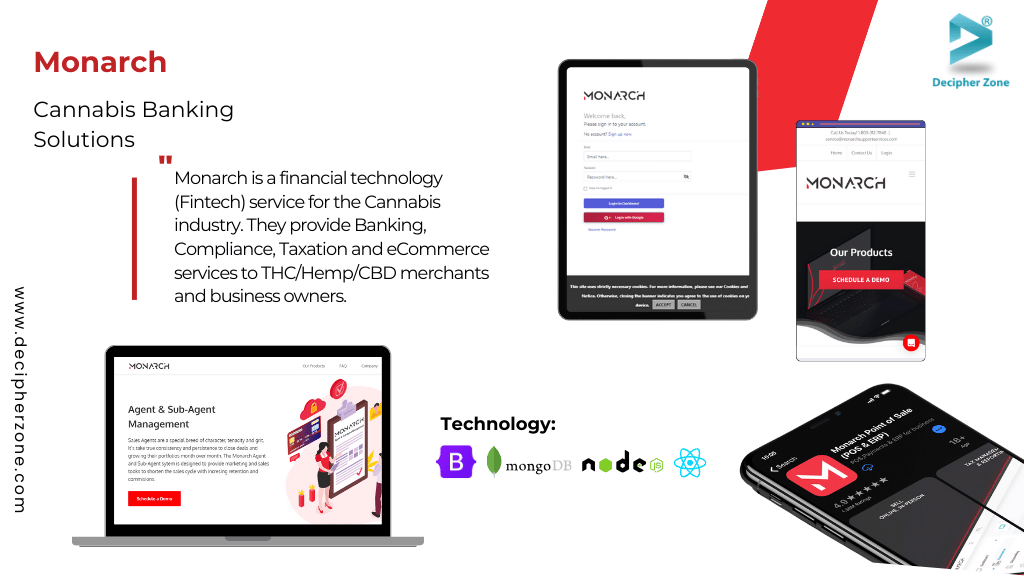

Monarch: Cannabis Banking and Digital Payments

The Challenge

The Challenge

Monarch provides a compliant digital banking solution for cannabis businesses and consumers in the US, where cannabis businesses face severe restrictions on traditional banking access. Monarch needed a secure transaction engine, strict KYC/AML procedures for every user, and jurisdictional tax payment automation for multiple US states simultaneously.

What We Built

- Secure transaction engine with licensed money transmitter compliance

- Identity verification integration with biometric matching and sanctions screening

- Mobile-friendly digital wallet for end customers

- Merchant web portal for payments, account monitoring, and reporting

- Automated jurisdictional tax calculation and remittance for each locale

- Compliance-first design with full transaction audit trails for regulators

The Outcome

Monarch has become a game-changer in a high-regulation environment. Cannabis dispensaries and related businesses now access banking functions that were otherwise unavailable to them.

Businesses send and receive digital payments (reducing all-cash operations), pay vendors digitally, and handle jurisdictional tax payments without manual calculation. The platform scales to additional US states because the compliance architecture was designed for multi-jurisdiction operation from the start.

Why Choose Decipher Zone for Retail Banking Software Development

.avif) Proven Experience Across Banking and Fintech

Proven Experience Across Banking and Fintech

We bring over a decade of experience in custom software development with a focus on financial services. Our portfolio demonstrates successful delivery of core banking systems, digital platforms, and fintech applications for clients across Africa, the US, the UAE, Saudi Arabia, and Europe. When you choose Decipher Zone, you get a partner that has encountered and overcome the specific challenges in banking projects, from complex legacy system integrations to stringent compliance testing requirements.

Domain Expertise in Banking Regulations and Fintech Innovation

Writing code is one thing. Understanding banking regulations across jurisdictions is another. Decipher Zone offers both. Our team includes subject matter experts familiar with PSD2, SEPA, RBI guidelines, AML/KYC requirements, and fintech innovation trends. We stay updated on the latest in digital banking so our solutions are not just technically sound but strategically aligned with where the industry is headed.

Tailor-Made Solutions Built for Your Competitive Edge

We understand that each bank or fintech has unique requirements, competitive differentiators, and regulatory environments. Selecting the right development partner means selecting one that specializes in custom software development, not one that forces an off-the-shelf product to work.

Our bespoke approach covers everything from UI design that matches your brand to architecture choices that align with your IT strategy, whether cloud-first, on-premise, or hybrid.

Full Lifecycle Partnership

Decipher Zone offers support at every step: initial consulting and requirements analysis, through development and testing, to deployment and post-launch maintenance. We assist with cloud setup, data migration from legacy systems, user training, and post-launch monitoring.

Many of our clients return for phase 2 enhancements or new projects as their needs grow, and this continuity translates into even better service over time as we accumulate deep knowledge about the business.

Quality, Security, and Compliance

Our internal processes are geared to deliver top quality in a domain where there is zero tolerance for errors or security lapses. We follow ISO-standard coding practices, conduct thorough QA, engage in third-party security audits, and comply with OWASP and CERT guidelines.

For payment projects we ensure PCI-DSS compliance. For personal data we adhere to GDPR or relevant local privacy laws. For US banking clients we meet FFIEC guidance requirements. In short, we treat your project with the same care as if we were building software for our own bank.

Competitive Pricing with Flexible Engagement Models

Decipher Zone offers cost-effective development at $25 to $49 per hour for senior engineers, without compromising quality. We work with startups on budget constraints and with enterprises providing dedicated development teams as an extension of your in-house team. Engagement models include fixed-price, time-and-material, and dedicated team, depending on what fits your situation best.

Get a free quote for your retail banking software project | Hire experienced banking software developers | Explore custom software development services

Frequently Asked Questions: Retail Banking Software Development

What is retail banking software development?

Retail banking software development is the process of designing, building, testing, and maintaining digital systems that power consumer-facing banking services. It covers core banking platforms (for handling deposits, loans, payments, and account management), customer-facing interfaces (mobile apps and web portals), compliance modules (KYC, AML, regulatory reporting), and integration layers connecting the bank to payment networks, fintech partners, and credit bureaus.

How much does it cost to build retail banking software?

Costs range widely based on scope. A basic mobile banking app costs $50,000 to $150,000 and takes 4 to 6 months. A full digital banking platform including mobile, web, KYC, and card management costs $200,000 to $600,000 over 8 to 14 months. A complete core banking system costs $800,000 to $2,000,000 or more over 12 to 24 months. At Decipher Zone, senior engineers work at $25 to $49 per hour, and every project starts with a discovery phase to scope requirements before production development begins.

Why choose custom banking software over an off-the-shelf solution?

Custom retail banking software offers tailor-made functionality aligned exactly with your business model and customer experience goals. You have full control over the feature set, architecture, and compliance implementation. Off-the-shelf solutions come with features you do not need (paying for bloat) or lack features that are critical to your specific market. Custom solutions integrate seamlessly with your existing systems and can be built with microservices architecture for long-term scalability. The competitive edge from software built specifically for your business is something generic platforms cannot provide.

How do you ensure security and compliance in banking software?

Security is embedded at every layer: AES-256 encryption for data at rest, TLS 1.2+ for data in transit, field-level encryption so database administrators cannot read payment details, and hardware security modules (HSMs) for key management. Compliance is built into the architecture from day one, not added afterward. This includes PCI-DSS for payment data, GDPR for EU personal data, BSA/AML for US requirements, and SOC 2 controls for enterprise service providers. Regular penetration testing, OWASP vulnerability scanning in CI/CD pipelines, and third-party security audits verify these controls in production.

How can fintech startups leverage retail banking software?

Fintech startups can use Banking-as-a-Service (BaaS) platforms or open APIs from licensed banks instead of building a full banking stack from scratch. A fintech integrates with a BaaS provider that offers modular banking services via APIs (account creation, payments, card issuance, KYC compliance), allowing the fintech to offer customers bank-like services under its own brand while focusing on its unique user experience. This dramatically lowers the barrier to market entry and reduces the compliance burden for a startup that does not yet have banking licenses of its own.

How long does retail banking software development take?

Timeline depends on scope. A simple banking mobile app interfacing with existing bank systems takes 4 to 6 months to design, develop, test, and launch. A full-scale digital banking platform (mobile app, web portal, KYC/AML, card management, customer support) takes 8 to 14 months. A complete core banking system with transaction ledger, product engine, and compliance reporting takes 12 to 24 months for an initial launch. Timelines extend for phased rollouts at large banks or when compliance requirements are discovered mid-build rather than scoped upfront.

What are the key 2026 trends in retail banking software?

The major trends shaping retail banking software development in 2026 are: AI and hyperautomation integrating machine learning into fraud detection, credit scoring, and customer onboarding. Central bank digital currencies (CBDCs) requiring new wallet and settlement infrastructure. Embedded finance enabling non-banking brands to offer financial products via BaaS APIs. FedNow and ISO 20022 driving real-time payment rail adoption. And biometric authentication replacing passwords as the primary security layer. Low-code platforms are also being adopted for non-core banking features to accelerate deployment timelines.

What technologies does Decipher Zone use for banking software development?

Decipher Zone primarily uses Java and Spring Boot for core banking backends due to their reliability and backward compatibility. Python is used for AI and machine learning modules including fraud detection and credit scoring. React and React Native power mobile and web banking interfaces. Cloud deployment uses AWS and Azure with Docker and Kubernetes for containerized microservices. For compliance and identity, we integrate Keycloak for IAM and implement AES-256 encryption with hardware security modules for key management. Apache Kafka handles real-time event streaming for transaction propagation across services.

Author Profile: Mahipal Nehra is the Digital Marketing Manager at Decipher Zone Technologies, specialising in content strategy and tech-driven marketing for software development and digital transformation.

Follow on LinkedIn or explore more at Decipher Zone.